The ₪1.1B Arnona reform battle. REE’s 99.8% Nasdaq wipeout. Cellcom lands AI dark fiber deal.

Today in Israel - and what it all means for the business community at home and abroad.

🍿 Get our coverage on Spotify, and Youtube, too. Want to join the conversation? We’re on X

Quick takes:

Macro & Policy: The Bank of Israel cuts its benchmark interest rate by 25 basis points to 3.50% amid easing geopolitical risk and stable inflation; An inter-ministerial clash erupts over the 2026 property tax reform.

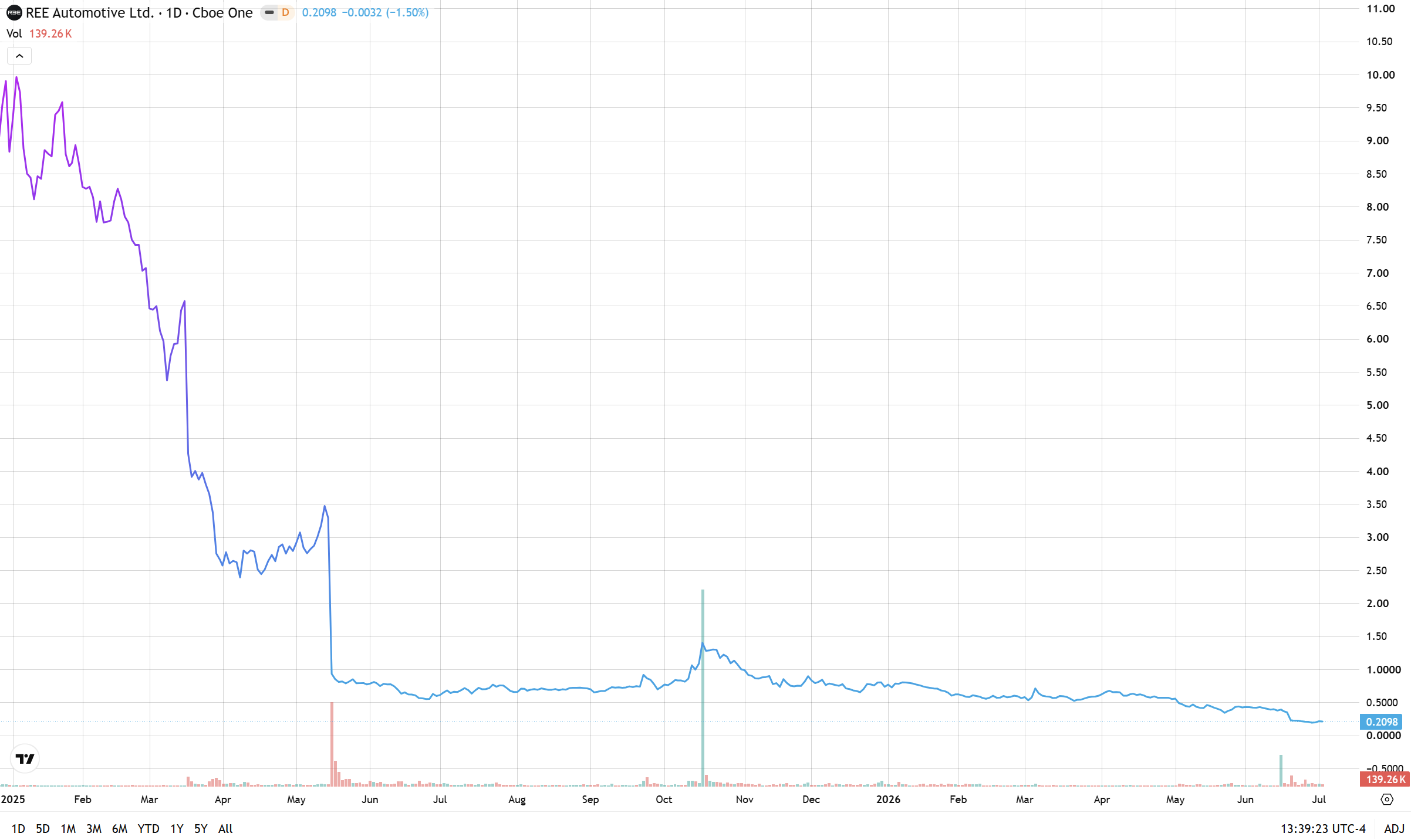

Automotive: EV startup REE Automotive files for a stay of proceedings in Tel Aviv with ₪51.5M in debt, ahead of its impending July 7 Nasdaq delisting.

Technology & Infrastructure: Cellcom secures a multi-million shekel contract to deploy dark fiber networks across Mega DC's data centers.

Macro & Policy

The Bank of Israel’s Monetary Committee, led by Governor Prof. Amir Yaron, reduced its benchmark interest rate by 0.25% to 3.50%, meeting market expectations. This follows a similar reduction in May. The central bank cited a stabilized geopolitical environment, bolstered by a US-Iran memorandum of understanding that drove Brent crude down 30% to ~$71 a barrel, and localized inflation remaining anchored at 1.9%, comfortably within the 1-3% target range. Furthermore, Israel's risk premium has retreated to pre-October 2023 levels. The BoI’s Research Department simultaneously updated its macroeconomic forecast, projecting a 4.0% GDP growth for 2026 and a robust 5.5% expansion in 2027. However, the labor market remains tightly constrained, with wage growth spiking 6.8% YoY between March and May.

Our take: Governor Yaron is executing a highly delicate monetary balancing act, capitalizing on a brief window of macroeconomic stability to stimulate a post-conflict recovery. The drop in the geopolitical risk premium and declining global energy costs have provided the BoI with the necessary arbitrage to ease borrowing costs without unanchoring inflation expectations.

However, the real friction lies in the looming specter of fiscal dominance. While the BoI projects a budget deficit of 4.9% for 2026, this heavily relies on the assumption that defense spending won’t overrun its current reserves. With a tight labor market driving a 6.8% wage inflation and military branches demanding an additional ₪25B, the central bank’s easing cycle is operating on borrowed time. If fiscal discipline falters or military mobilization expands, the BoI will be forced into a hawkish reversal to combat supply-side inflationary pressures.

An inter-ministerial rift has emerged over the 2026 municipal property tax (Arnona) discount reform. The Ministry of Finance's Chief Economist issued a warning that the revised criteria, which expands eligibility by 100,000 households to a total of 840,000, will inject a ₪1.1B burden onto municipal budgets. The Treasury argues this structurally threatens the financial stability of weaker municipalities and introduces negative employment incentives, noting that 20% of the newly eligible fall into middle-income deciles. In contrast, Interior Ministry Director-General Yisrael Ozan defended the reform, arguing that linking income tests to the minimum wage corrects a long-standing distortion. Ozan noted that the regulations only set a maximum discount ceiling, leaving municipalities with the autonomy to adjust actual discounts and prevent structural deficits.

Our take: The Treasury might be right to signal the alarm on the macroeconomic ripple effects of this policy. Shifting a ₪1.1B fiscal burden onto local municipalities without a corresponding centralized funding mechanism could cause a dangerous structural imbalance. Weaker municipalities, already suffering from an inferior ratio of high-yield commercial Arnona to loss-making residential Arnona, will be forced to either slash vital services or seek government bailouts, exacerbating existing inequalities across OECD metrics. Furthermore, by flattening the discount model without a strict taper rate tied to workforce participation, the state risks institutionalizing an arbitrage where the marginal utility of additional labor income is negated by the loss of tax subsidies. Institutional resistance to this reform from local mayors will likely be fierce, as it represents a classic misallocation of capital masquerading as social policy, threatening local balance sheets at a time of heightened macroeconomic vulnerability.

Automotive

EV platform developer REE (NASDAQ: REE) Automotive is scheduled to be delisted from the Nasdaq in two days, on July 7, 2026, marking a devastating 99.8% value destruction from its $3.1B SPAC valuation five years ago. Currently trading at a market capitalization of just $6M, the company has filed an urgent request for a stay of proceedings with the Tel Aviv District Court to freeze its ₪51.5M debt, comprising ₪12.2M owed to employees and ₪39.3M to general creditors. Represented by Herzog Fox & Neeman, REE is seeking to appoint a settlement manager to restructure. Management attributes the severe liquidity crisis to overwhelming macroeconomic headwinds, including US tariff policies and a frozen capital market for EV startups, heavily compounded by local geopolitical instability that deterred foreign direct investment.

Our take: REE’s spectacular implosion is a textbook case of the zero-interest-rate policy (ZIRP) hangover colliding with brutal geopolitical realities. Like many mobility SPACs of its vintage, REE went public on a narrative of an infinite total addressable market (TAM) rather than near-term cash flow or solid EBITDA margins. As the cost of capital normalized, the market rapidly repriced the immense cash burn required to bring hardware platforms to commercial scale.

Technology & Infrastructure

Cellcom (TASE: CEL) has inked a multi-million shekel agreement with Navius to provide critical communication infrastructure for AI data centers operated by Mega DC, a subsidiary of the Mega Or Group. The telecom operator will deploy a Dark Fiber network connecting three primary data centers in Beit Shemesh, Masmiya, and Modi'in. The infrastructure includes highly secure backup routes and direct connectivity to the Israeli Internet Exchange (IIX). Cellcom CEO Eli Adadi emphasized that this high-capacity, low-latency connectivity is essential for neo-cloud players and AI processing, positioning Cellcom directly in the middle of Israel’s AI infrastructure buildout.

Our take: This deal underscores a structural shift in Israel’s telecom sector. The pivot from traditional retail mobile margins to enterprise-grade AI infrastructure. As global cloud hyperscalers and local operators scramble for compute capacity, the friction is no longer solely about GPU chip supply, but rather the physical data transport and latency required for high-performance computing (HPC).

Cellcom is leveraging its existing infrastructure arbitrage to capture a slice of this highly lucrative market. By laying the ‘dark fiber’ pipelines between regional data centers, legacy telcos are effectively positioning themselves as the toll collectors of the AI boom, buffering their balance sheets against domestic consumer market stagnation and the oligopoly of consumer tech.

TASE snapshot for Monday, July 06, 2026

TA-35 Index (TASE:TA35): 🟢 +1.05%

TA-90 (TASE:TA90): 🟢 +1.25%

TA-125 (TASE:TA125): 🟢 +1.10%

If you enjoyed this update, forward it on.

TV10 Global | Israel for Investors

Bringing you the top stories from the Israeli business community, by Israel’s only business and finance network.

Share your thoughts with us via: global@tv10.co.il or the Newsroom WhatsApp: +972-55-994-5851.

📧 Subscribe to this newsletter! And follow the daily conversation on 𝕏 @tv10global.

Disclaimer: This brief is for informational purposes only and does not constitute investment advice. All data current as of publication date.